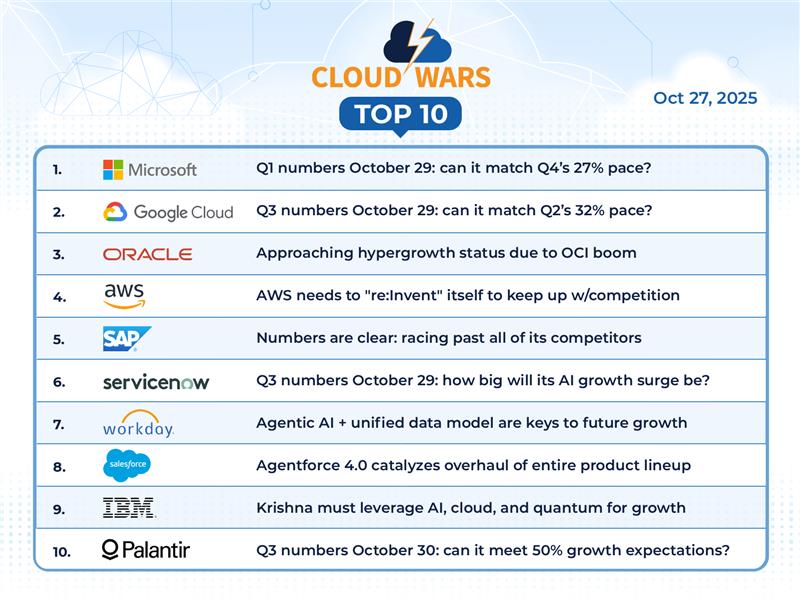

As the enterprise-applications business undergoes radical transformation with the infusion of agentic-AI capabilities, SAP remains the fastest-growing player in the field by far, outpacing longtime rivals Oracle and Salesforce by more than 100% and Workday by about 60%.

The rapid and intense shift toward AI agents has likely caused some confusion and hesitation among business customers who, after a few decades of spending many billions on and getting comfortable with traditional applications, are now trying to fully comprehend the impact of this powerful and highly disruptive new technology.

Despite that measure of uncertainty — and SAP might suggest that it’s precisely because of that uncertainty — SAP continues to pump out results that clearly demonstrate its leadership in the space. Here are the enterprise-apps revenue figures and growth rates for the most-recent quarter for the four major players:

- SAP: $6.14 billion, up 22%

- Workday: $2.17 billion, up 14%

- Oracle: $3.8 billion, up 11%

- Salesforce: $10.2 billion, up 10%

Another indication of SAP’s ongoing strength are the results for its Cloud ERP Suite, which are included within the overall Q3 cloud-apps number of $6.14 billion. For Q3, the Cloud ERP Suite business was up 26% to $5.32 billion.

AI Agent & Copilot Summit is an AI-first event to define opportunities, impact, and outcomes with Microsoft Copilot and agents. Building on its 2025 success, the 2026 event takes place March 17-19 in San Diego. Get more details.

I’m aware that some analysts tend to dismiss the growth-rate discrepancies because they believe SAP has a “captive” market made up of its 20,000 on-premises customers who are being given big incentives by SAP to make the move to the cloud. But while SAP certainly has, by virtue of its incumbent position with those 20,000 customers, a distinct advantage in competing for the next-step cloud business, those customers are no doubt drawing intense interest from Oracle, Salesforce, and Workday for those big opportunities.

But in spite of that, SAP continues to outperform its rivals by an enormous margin, a trend that has held steady for at least the past four quarters.

One other area in which SAP continues to post excellent results is “current cloud backlog.” For Q3, that number — which is the equivalent of what some companies refer to as RPO, or remaining performance obligation — was $18.1 billion, up 23%.